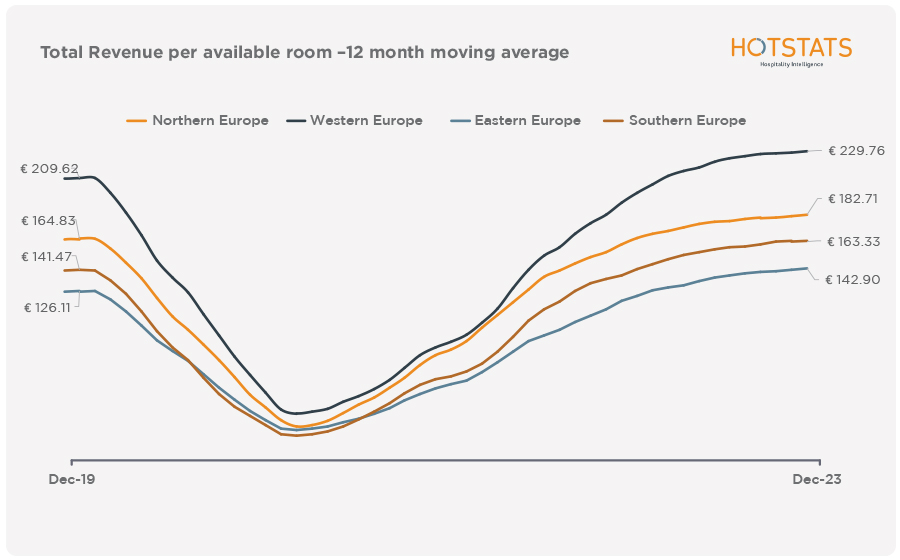

2023 was an incredible year for European hotels. From a top-line perspective, ADR growth of 6.9% year-on-year and an occupancy uplift of 6.6 percentage points saw RevPAR grow a massive 18.3%.

Of course, with first quarter 2022 being still dominated by the effects of COVID-19, Q1 2023 YOY TRevPAR growth was 57.2% and GOPPAR went from €13.97 to €34.67 (+148.2%). The remaining three quarters saw milder growth of 10.1% in TRevPAR and 9.5% in GOPPAR.

More recently, the rate of revenue growth has slowed. Q4 showed growth year on year of 5.5% in TRrevPAR and 2.9% in GOPPAR, a potential sign that we are heading back to pre-pandemic levels of annual growth. One thing is certain, European hotels are in a much better position than many predicted 18 months ago. ADR is up 27.8% compared to 2019 and there are no immediate signs that this will fall any time soon.

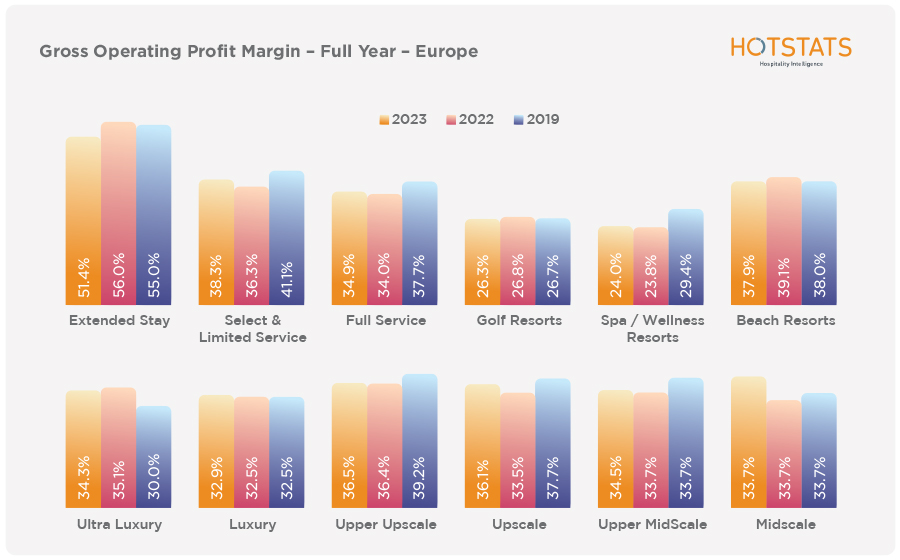

Unfortunately, the revenue and ADR growth seen in Europe has not converted directly to margin improvements across the board. High inflation, surging energy prices, supply-chain challenges and rising labor costs have softened margins and eaten up much of the rate growth. Amsterdam, for instance, saw 33% growth in revenue and no movement in margin. Prague coming from a low base and over 35% revenue growth achieved the highest margin growth, although still 4.3 percentage points short of 2019.

Extended-stay properties across Europe struggled to continue the incredible performance over the preceding years, with ADR growth the slowest of the asset classes. The select- and limited-service segment performed the best with a 2-percentage point YOY improvement. This was related to the size of the demand growth, with a more limited impact on the cost lines, driven by large amounts of clustering and centralizing of costs and smaller operating models.

Year over year, the lower end of the chain scale has seen the largest improvement in profit margin. Midscale, in particular, saw a 6.7-percentage-point increase over this period. Ultra-luxury saw a drop in margin, with luxury and upper-upscale segments holding flat YOY. Much of this relates to the lower change in average daily rate, but also challenges in operating costs, which the higher-end hotels are more exposed to.

Another factor is the ongoing challenge around F&B profitability. Although the year-on-year change is minimal compared to 2019, most of Europe has seen a significant fall in profit. Supply chain issues, driven by the rising cost of transportation and energy, combined with labor costs surging, have all contributed.

Revenue growth of 3.4% per occupied room in the food and beverage outlets, combined with slow recovery of conferencing and events, has meant that costs have risen significantly faster and greater than guest spend.

Guests have increasingly more options outside of hotels, combined with the increased ability to be able to order to their room using food-delivery apps. Hotel F&B is at the forefront of topics in Europe as hoteliers work to balance guest’s changing habits with trying to find a way to keep F&B profitable.

Guests have increasingly more options outside of hotels, combined with the increased ability to be able to order to their room using food-delivery apps. Hotel F&B is at the forefront of topics in Europe as hoteliers work to balance guest’s changing habits with trying to find a way to keep F&B profitable.

Hotels in France are barely profiting on average in F&B and Belgian hotels saw a fall of 11.9 percentage points since 2019, a 3-percentage-point impact on total hotel profit margin.

The wider consideration for European hotels is how the various revenue centers complement ADR and the overall total revenue picture. Wellness (spa and health club) revenues, for instance, continue to thrive, replacing some of the loss of F&B profit and driving guest spend. Rooms department profit contribution is also holding strong at 72% on average for Europe, the result of average rate growth achieved across the board.

Looking ahead, revenues are slowing, but there are positive signs that costs are, too, with many industry players predicting a pre-pandemic level of growth closer to the rate of inflation.

Story contributed by Michael Grove, COO, HotStats.