When the effects of COVID-19 ravaged the world’s travel industry starting at the beginning of 2020, none of us thought it would last so long. However, only recently did the World Health Organization announce its official end as a pandemic; it’s time we all moved on.

China had been both a puzzle and a rollercoaster for the hotel industry, domestically and globally due to its massive impact as an outbound market. For example, prior to COVID, travelers from China accounted for almost a third of all international visitors to places such as Japan and Thailand, two of the most visited destinations on the planet.

The infamous zero-COVID policy plagued the entire world with supply-chain issues, completely closed off borders for entry into mainland China and continued to hurt the nations trying to recover without the millions of Chinese guests.

When Chinese officials suddenly announced an end to the policy in January 2023, it was met with joy: the hotel industry has been one of the last major sectors to return to normality.

Hotels manned up and got ready at a moment’s notice to welcome the influx of guests that was surely to follow, especially for the Chinese New Year holidays toward the end January. The mood was exuberant.

Three weeks later, it dawned on everyone that all that excitement was misguided, as outbound travel faltered due to a variety of reasons. Chinese travelers were vaccinated by the Sinopharm and Sinovac vaccines, which are largely unrecognized internationally. Even if a vaccine certificate was not required, Chinese people themselves were worried because of the lower efficacy of their doses. Also, airlines need much longer time to rebound when compared to hotels due to the mandatory training for cockpit and cabin crews. Lastly, flights were exorbitantly expensive.

Thailand did, however, manage to receive 150,000 visitors from China in February 2023, but as large as this number seems, it is still 85% lower than 2019 numbers. Japan and Korea fared even worse as they barely managed just 5% of 2019 volumes.

Improvements are being made as the number of daily outbound flights has increased from 200 in November 2022 to 800 by the beginning of May 2023. For comparison purposes, these numbers were just a hair under 3,000 flights a day heading out of China in 2019. Clearly, the numbers are still way off.

GETTING HEALTHIER

What does all this mean for the hotel industry performance in mainland China?

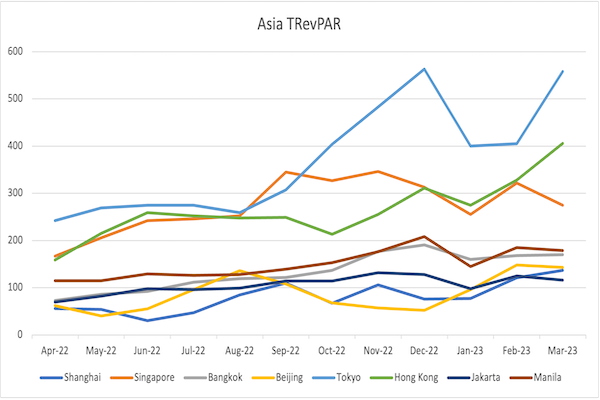

To fully understand this is to look at a metric that covers total performance: TRevPAR, or total revenue per available room, which encompasses all revenue—rooms and ancillary—generated by a hotel. The data for this insight is provided by HotStats, which collects full profit-and-loss data from almost 11,000 hotels globally.

Tokyo looks like the clear leader, but that’s mainly due to higher average rates, which the market has traditionally demanded. Singapore was running second with very respectable and constantly growing numbers and, in a close third, Hong Kong also seemed to be doing fine; however, it’s a bit of an illusion as its numbers fall far behind what is deemed normal.

At the same time, both Shanghai and Beijing, whose performance is accepted as a clear indication of the entire country, were running at an average of $50 USD less than a fifth of what Singapore, Hong Kong and Tokyo managed. The reason is a series of ultra-strict lockdowns that virtually paralyzed the nation. Some would argue that these measures worked as the caseloads remained low. July and August saw TRevPAR figures rising to over double what was done earlier in the year.

This seemingly magical and instant resurgence had been a hallmark of China’s hotel industry performance for the past three years. Once restrictions ease, people leave their homes and go to hotels. But then, come October and November, another round of lockdowns came along, which were especially hard on Beijing hotels and numbers crumbled again. This time to less than a tenth of what Tokyo managed in the same period.

On a more optimistic note, we need to look at the performance of these two key Chinese cities in Q1 2023. The growth is immense and stable hitting TRevPAR of $140 USD, almost tripling from just 10 months previous. Growth will continue its gradual climb up as international confidence and seat capacities return on flights, both in and out of the country.

The dragon has awoken. Now let’s see how it does for the rest of 2023 and beyond. The eyes of the world are on it.

Story contributed by Tareq Bagaeen, founder of aQedina.com, a comprehensive commercial resource to hoteliers. He is also a consultant with benchmarking firm, HotStats.