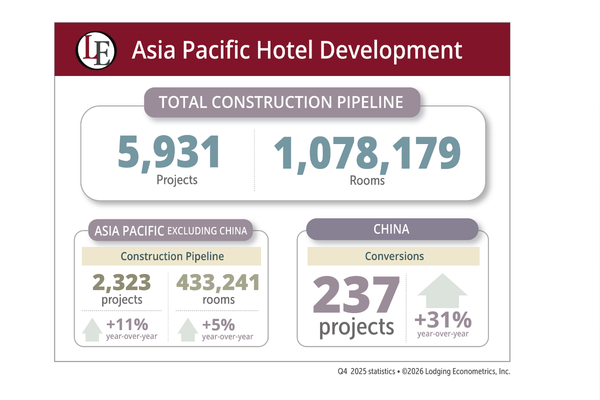

Glance at a map of hotel development activity and one thing becomes immediately clear: Asia Pacific, with 5,931 projects and 1,078,179 rooms, accounts for a massive share of worldwide new construction. But the real story isn’t just scale; it’s that Asia Pacific’s two largest areas—China and the rest of the region—are growing in fundamentally divergent ways. The upshot: Both strategies are reshaping the competitive landscape for years to come.

What’s happening across Asia Pacific right now is remarkable in its breadth. India is driving project growth at a rate not previously seen, hotel owners in China are rethinking their existing assets through record brand conversion activity and luxury development is surging across Southeast Asia. These aren’t isolated trends—they’re converging to make this a consequential region in global hospitality development.

New-Build Boom Outside China

The numbers outside China tell a story of acceleration. The pipeline in Asia Pacific, excluding China (APEC), climbed 11% year-over-year (YOY) to 2,323 projects—a record-high count—accounting for 433,241 rooms, up 5% YOY. What makes this especially notable is that early planning activity jumped 19%, suggesting that the expansion still has a significant runway. When early-stage pipeline activity rises this sharply, it typically signals that developers and brand partners are aligning on projects that won’t break ground for at least a year, reinforcing confidence in the region’s long-term demand.

India is the headline. With 906 projects now in its pipeline—a 31% year-over-year increase—the country alone represents 39% of all APEC development. That’s a staggering concentration of activity for a single country and it reflects both domestic travel demand growth and international brand confidence in India’s hospitality trajectory. A rising middle class, expanding flight connectivity and government investment in tourism infrastructure are all fueling the pipeline. Meanwhile, Japan’s pipeline grew 23% by projects, with Tokyo nearly doubling its project count year-over-year—a remarkable acceleration driven in part by record inbound tourism and favorable exchange rates that have made the country an attractive destination for international visitors. Vietnam, Indonesia and Thailand round out the top five countries in the APEC region, with Bangkok maintaining its position as the most active city for development.

The chain scale mix reveals where brands are placing their bets. Luxury, upper-upscale and upscale segments all reached record-high project counts across the APEC region, with luxury alone climbing 14% year-over-year. This tilt toward premium hotel development projects suggests that APEC developers are seeing a traveler base in Asia Pacific that’s increasingly willing to pay for higher-quality hotel experiences. For hotel vendors, owners and franchise companies targeting this corridor, the opportunity is squarely in the upper tiers of the market.

The China Pivot

China’s development story reads differently. The total pipeline of 3,608 projects and 644,938 rooms has held relatively steady, but underneath the surface, something significant is happening. Existing hotel conversions hit a record 237 projects—a 31% year-over-year jump—signaling that China’s hotel market is entering a new phase. Owners are increasingly choosing to rebrand and reposition existing properties.

This is a sign of a maturing market. When owners start investing heavily in conversions rather than ground-up construction, signals they’re focused on optimizing returns from existing real estate. They’re choosing their brand partners carefully, targeting specific chain scales, and betting that the right brand on an upgraded property can unlock demand that an independent hotel simply can’t capture.

New construction hasn’t stalled altogether. China still delivered 970 hotel openings in 2025 alone, far outpacing any other single country globally. The upper-midscale and upscale segments, which together account for 64% of China’s pipeline, are where the bulk of the activity is concentrated. Cities including Chengdu, Guangzhou and Shanghai continue to anchor the pipeline, while second-tier cities, such as Hangzhou and Xi’an, are contributing meaningful project counts of their own, reflecting the geographic broadening of China’s hospitality development beyond its primary gateway cities.

What It Means

Taken together, the two halves of Asia Pacific present a compelling picture for hotel vendors, franchise companies and ownership groups. In the APEC countries, the opportunity is in building new—getting into fast-growing markets, such as India and Japan, partnering on luxury and upper-upscale projects and positioning for a wave of openings that Lodging Econometrics forecasts will deliver nearly 700 new hotels across 2026 and 2027 combined. In China, the opportunity lies in conversions and renovations, working with owners who are actively seeking brand partnerships to reposition their portfolios and maximize returns on existing assets.

Across the full region, more than 1,300 hotels opened in 2025, with many more scheduled for 2026 and beyond. For anyone in the business of supplying, financing or operating hotels, understanding this pipeline at a granular level isn’t optional—it’s essential. The scale, diversity and strategic complexity of Asia Pacific’s development landscape make it one of the most important stories in global hospitality today.

Story contributed by Bruce Ford, SVP & director of global business development, Lodging Econometrics.