Despite solid revenue numbers, European hotels now confront a new reality: stagnating margins and weakening profit conversion signal the end of the post-pandemic boom.

Still, the headline numbers coming out of Europe’s hotel sector look respectable. Revenues are ticking up, demand hasn’t collapsed, but dig deeper into P&L statements and a troubling pattern emerges: Profit margins have stopped expanding, cost pressures—particularly labor—are becoming structural, and the ability to convert incremental revenue into profit is weakening. In sum, the engine that powered the post-pandemic profit surge is sputtering.

Recent performance data across Europe illustrates why this shift matters.

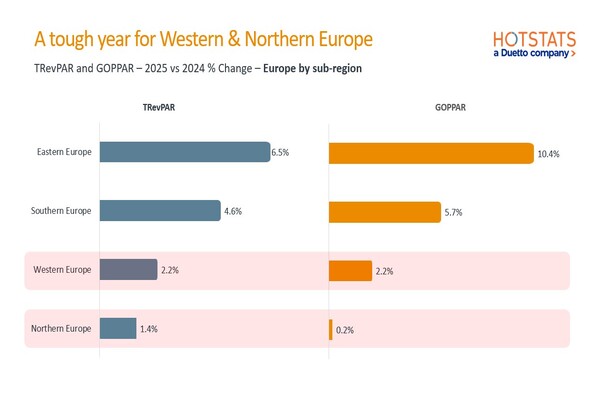

REVENUE GROWTH IS UNEVEN— AND INCREASINGLY REVEALING

Across Europe, revenue growth continues, but not evenly. Eastern Europe remains the strongest performer, with TRevPAR up 6.5% and GOPPAR up 10.4% year-on-year. Southern Europe follows with more moderate growth of 4.6% and 5.7%, suggesting the region has moved beyond recovery and into normalization.

By contrast, Western and Northern Europe are showing signs of strain. TRevPAR growth is limited to 2.2% and 1.4%, while GOPPAR growth slows to 2.2% and just 0.2%, respectively. Revenue momentum is weakening even as cost pressures, particularly labor, continue to rise.

This divergence reinforces a broader shift in performance measurement. RevPAR alone no longer captures the full revenue picture. As hotels seek growth beyond rooms, TRevPAR has become a more meaningful indicator of overall performance.

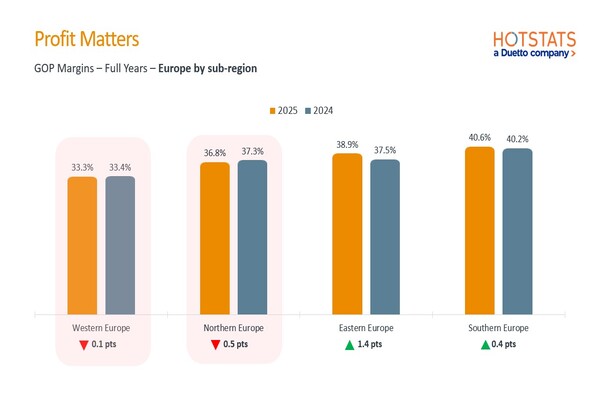

MARGINS HOLDING; NOT EXPANDING

Looking beyond revenue, Europe’s profitability story becomes more constrained. GOP margins in full-year 2025 stand at approximately 36.5%, broadly in line with last year. While still healthy by historical standards, margin expansion has stalled.

Southern Europe continues to lead, with GOP margins approaching 41% and remaining stable around 40% since 2023, now slightly above pre-pandemic levels. Western Europe sits at the opposite end of the spectrum, posting the lowest GOP margin at 33.3%, still below pre-pandemic performance.

Revenue growth alone is no longer delivering margin expansion. Profitability increasingly depends on how effectively operators convert revenue into profit.

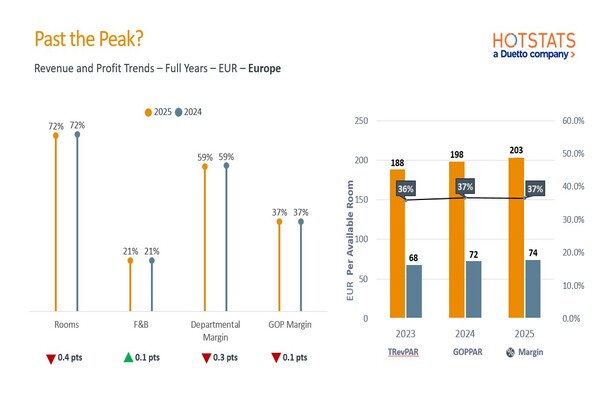

PEAK PROFITABILITY?

PEAK PROFITABILITY?

At an aggregate level, Europe may already have passed its profit peak. GOP margins rose steadily through the recovery and reached a high point in 2024. In 2025, margins remain strong at just under 37%, but the trajectory has flattened.

This is happening despite continued top-line growth. Both TRevPAR and GOPPAR are up by nearly 3% year-on-year. However, flow-through is running at only 35%, meaning incremental revenue is delivering significantly less incremental profit than in earlier years.

The next phase of performance will depend less on demand recovery and more on operational discipline.

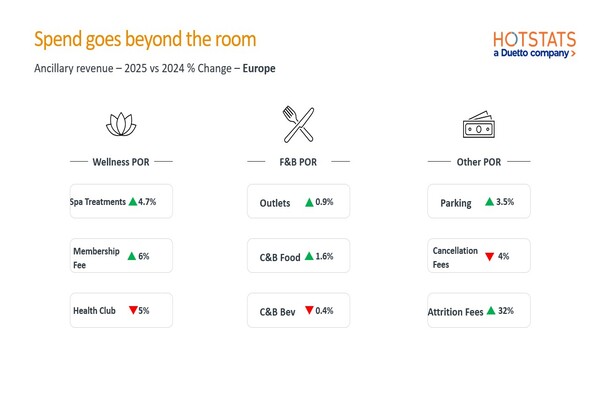

ANCILLARY REVENUE MOVES CENTER STAGE

As room revenue growth moderates, ancillary income is becoming increasingly important. Wellness stands out, with spa treatments and membership fees up 4.7% and 6%, reaching approximately €10–€11 per occupied room.

Food-and-beverage performance is more mixed. Outlet and C&B food revenues show modest growth, while beverage revenues remain under pressure, highlighting the need for targeted activation rather than broad-based pricing. Other revenue streams, such as parking and attrition fees, continue to rise.

Incremental profit today is less about selling more rooms and more about maximizing spend across the entire property.

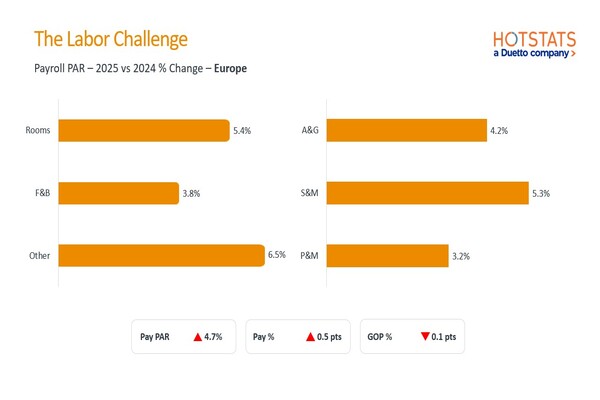

RESHAPING THE P&L

Labor has become the single largest pressure point on profitability. Total payroll per available room is up nearly 5% year-on-year, driven by increases across Rooms, F&B operations, and Sales & Marketing. Labor inflation is no longer cyclical—it is structural.

Pressure extends further down the P&L. Credit card commissions now average €3 per available room, up from €2.3 pre pandemic. Sales & Marketing expenses remain elevated at €2.3 PAR as operators work harder to drive incremental revenue, while rising loyalty program costs— driven by increased points issuance and promotions—continue to erode margins.

WHAT COMES NEXT

WHAT COMES NEXT

Europe’s hotel sector has moved beyond recovery and into an optimization phase. Revenue is still growing, but margins are flat, costs are structurally higher and profit conversion is under strain. What comes next will be defined by operational precision, not demand growth.

“Hotels that succeed in this environment will be the ones that understand profit at a granular level,” said Michael Grove, CEO of HotStats. “That means knowing exactly where revenue is generated, where costs are rising and where action will have the greatest impact.”

In today’s market, profitability is no longer about chasing growth—it is about precision profit engineering.

This story was contributed by Juan Gallardo and Jeannette King of HotStats. HotStats, now a Duetto company, is a global data benchmarking company for the hospitality industry.