The narrative that the U.S. hotel single-sale transaction market has been in a deep, slow slump is largely untrue. Though sale transaction volumes have not set record highs, the market has demonstrated remarkable resilience despite headwinds, such as elevated interest rates.

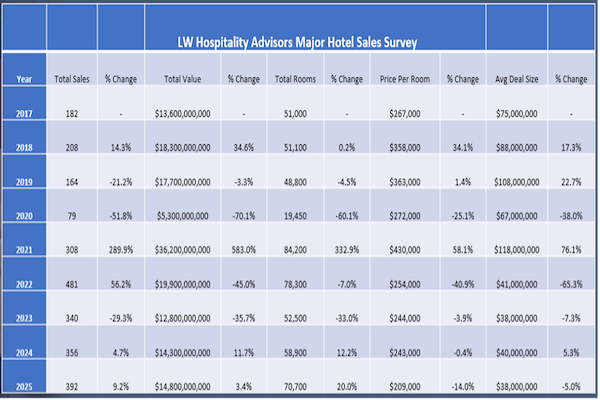

A review of the “LW Hospitality Advisors Major U.S. Hotel Sales Survey” (single sale transactions over $10 million) during the past nine years yields interesting conclusions:

Between 2017 and 2019:

- Total number of trades ranged between 164 and 182 properties

- Total number of rooms sold ranged between 48,800 and 51,100

- Total dollar volume sold ranged between $13.6 billion and $18.3 billion

- Sale price per room sold ranged from $267,000 and $363,000

- Average deal size sold ranged from $75 million to $108 million

2020, the year of the COVID pandemic, was an anomaly:

- Total number of trades was 79—a 52% decrease compared with 2019

- Total number of rooms sold was 19,450—a decline of 60% compared with 2019

- Total dollar volume sold was $5.3 billion—a decline of 70% compared with 2019

- Sale price per room sold was $272,000—a 25% decrease compared with 2019

- Average deal size sold was $67 million—a decline of 38% compared with 2019

2021 was also an anomaly as the COVID-19 pandemic entered a complex phase characterized by the dual emergence of life-saving vaccines and more contagious viral variants like Delta and Omicron. While 2020 was defined by initial lockdowns, 2021 saw a transition toward phased reopenings and a shift in how the world managed the virus.

As swiftly as the pandemic led to widespread closures and cancellations beginning in March 2020, signs of an equally robust recovery were percolating with expectations of the strongest growth ever in key lodging industry metrics. A wave of loan defaults impacted the lodging industry with lenders and servicers considering forbearance and loan modification asks. Numerous hotel bankruptcies led to a trend that was anticipated to increase as owners of struggling assets were unable to pay their debt service.

During this time there was an extraordinary amount of liquidity in the market, particularly relative to limited availability of opportunities. Domestic and international private equity funds, hedge funds and high-net-worth investors, along with U.S. REITs, were actively pursuing prospects to deploy capital at an attractive basis, as the disparity between assets with capital needs and depth of money sources seeking to invest in lodging assets was never greater.

In 2021, the U.S. hotel sale transaction market gained traction and with the accumulation phase of a new market cycle having clearly begun, sophisticated contrarian-minded investors perceived epic near-term appreciation potential.

In 2021:

- Total number of trades was 308—a nearly four-fold increase compared with the prior year

- Total number of rooms sold was 84,200—roughly 73% greater when compared with 2019

- Total dollar volume sold was $36.2 billion—a nearly two-fold increase compared with 2019

- Sale price per room sold was $430,000—an 18% increase compared with the prior year

- Average deal size sold was $118 million—a 9% increase compared with 2019

Between 2022 and 2025:

- Total number of trades ranged between 356 and 481 properties

- Total number of rooms sold ranged between 52,500 and 78,300

- Total dollar volume sold ranged between $12.8 billion and $19.9 billion

- Sale price per room sold ranged from $209,000 and $254,000

- Average deal size sold ranged from $38 million to $41 million

It is noteworthy that during 2025:

- Except for 2022, the total number of trades of 392 was the largest amount realized during the past nine years

- Total number of rooms sold of 70,700 was greater than the amounts achieved between 2017 and 2020, as well as in 2023 and 2024

- Total dollar volume sold of $14.8 billion was greater than the amounts achieved during 2017, 2020, 2023 and 2024

- Sale price per room of $209,000 was the lowest amount realized during the past nine years

- Average deal size of $38 million, which equaled the same amount during 2023, was the lowest amount achieved during the past nine years

In summary:

- The total number of trades between 2021 and 2025 eclipsed the numbers that occurred between 2017 and 2019

- Total dollar volume between 2023 and 2025 is within a similar range to what occurred between 2017 and 2019

- The sale price per room between 2022 and 2025is significantly below what was achieved between 2017 and 2020

- Average deal size between 2022 and 2025 was below what occurred between 2017 and 2020

During the recent past, while the U.S. hotel sale transaction market has not been in a deep slow slump, sale price per room and average deal size remain below pre-pandemic levels.

The current landscape in the hospitality sector presents a rare, time-sensitive and compelling opportunity for a run-up in sale transaction activity and property values. Supported by sustained travel demand and steady performance trends, lodging facilities are one of the most resilient and profitable commercial property types and desirable assets for investors seeking portfolio diversification and long-term value.

Daniel Lesser is co-founder, president and CEO of LW Hospitality Advisors, an asset management firm based in New York.