A capitalization rate, or cap rate, is a ratio that can be used to estimate the value of income-producing properties. Put simply, a cap rate is the percentage of net operating income (NOI) to property asset value. For example, a $10 million sale price of a property that produces an annual net cash flow of $900,000 results in a calculated capitalization rate of 9.0% ($900,000/$10,000,000).

A comparatively lower cap rate indicates less risk associated with an investment, while a relatively higher cap rate points toward more risk. Factors considered in assessing risk include creditworthiness of a tenant; term of lease; durability of the income stream; quality and location of the property; capital markets/debt availability; and general volatility of the market.

Use of a cap rate implies a durable and stable income stream, either in place or projected. It is important to note that unlike investors of other types of commercial real estate, such as office and multifamily, sophisticated hotel investors do not typically formulate pricing decisions using a single cap rate applied to one year’s NOI, whether actual or anticipated. Given the lack of long-term leases and the unique feature of a continuous re-pricing of the leasing of transient hotel rooms, theoretically, lodging assets never stabilize.

Cap Rates: Fair or Foul?

Literally, not a day goes by without my being asked by someone about the reasonableness of a deal capitalization rate. My standard response is: “Before I answer, which cap rate are you referring to? Trailing 12 months in place actual, projected year one, stabilized year or stabilized year deflated to today. Then, which level of income? Gross Operating Profit Before Management Fee(s) and Reserve for Replacement (Reserves); NOI after Base Management Fees; NOI after Base & Incentive Management Fees; NOI after Base & Incentive Management Fees and Reserves. Further, what percentages of revenues are being allocated to Base Management Fees, Incentive Management Fees, and/or Reserves?”

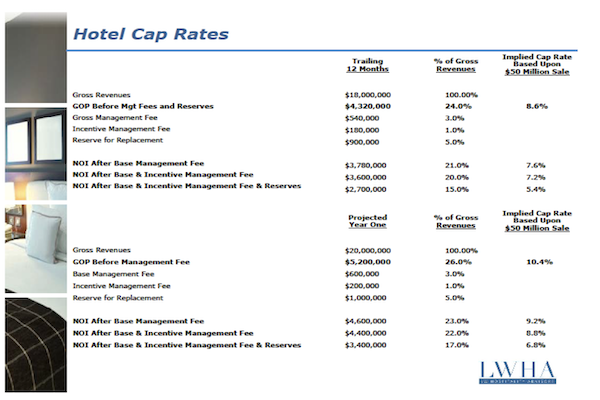

To illustrate the point, consider the eight different cap rates derived from a $50 million sales price of a 200-room, full-service hotel:

As illustrated, the range of 5.4% to 10.4% is very wide and proves the dramatic sensitivity of cap-rate calculations and the need to establish the year and level of net income, which are to be considered for such an analysis. If not, one may be mixing apples with oranges. When analyzing a lodging transaction, the story/detail behind the NOI level being utilized must be developed to truly comprehend what in fact the cap rate is.

It is critical to note that while many commercial property types produce relatively stable annuity type income, transient lodging facilities house operating businesses with volatile short-term and, in many cases, various divergent, revenue streams (i.e. rooms, food, beverage, recreational).

Furthermore, hotel investors are generally an optimistic group who seek value-enhancement opportunities. To establish pricing, hotel sponsors primarily rely upon a discounted-cash-flow (DCF) analysis that factors in their perceived upside during an assumed holding period. In practice, the value conclusion produced by a DCF analysis for a lodging asset is then used to “reverse engineer” an implied cap rate or rates based upon historic actual and/or projected NOI and is merely considered a “back of the envelope” benchmark consideration.

Throughout my career, I have come across terrific lodging investment opportunities priced at 2% cap rates as well as terrible deals available at 10% cap rates. For example, I have seen low-cap-rate deals that reflect investment at a fraction of replacement cost indicating potential upside through a successful business plan. Alternatively, I have encountered high-cap-rate deals that reflect asset value meaningfully greater than replacement cost with substantial downside risk associated with factors such as new supply coming into the market and/or demand generators relocating.

The bottom line: Relying solely on cap rates to value a hotel asset is fraught with danger and does not reflect the actions of sophisticated lodging investors.

Daniel H. Lesser is co-founder, president, & CEO of asset management company LW Hospitality Advisors.