As the Chinese market recovers from the pandemic, important trends have been noticed in the Mainland China market.

Contributed by Julie Dai, Horwath HTL, Beijing

Here is our perspective:

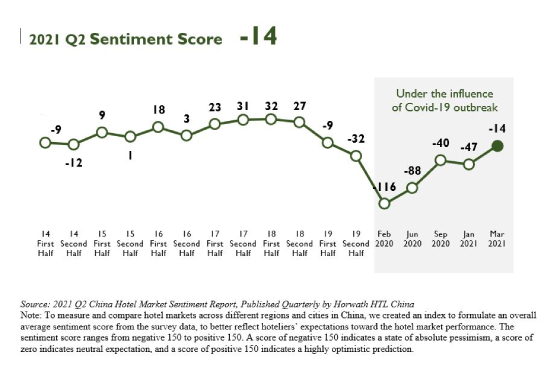

The market emerged from the downturn and showed a strong recovery: Since the COVID-19 outbreak in early 2020, the global and Chinese hotel industries have experienced significant negative impacts. Thanks to the strong control measures of the Chinese government, the epidemic in the mainland of China has been controlled relatively quickly, thus supporting the strong recovery of the mainland hotel market. In the second half of 2020, most markets across the country have entered the path of recovery. The chart below shows the changes in the sentiment score of the hotel market in Mainland China since the outbreak of the epidemic.

Domestic tourism demand shows the strongest recovery: Due to the temporary closure of outbound tourism, domestic tourism has shown the strongest recovery, especially in popular resort and tourism destinations (Hainan, Yunnan, Northeast China). Particularly, high profile and luxury resort hotels located in these areas reported higher performance results in 2020. In addition, suburb resorts with the three major economic circles (the Yangtze River Delta (YRD), the Greater Bay Area and the Bohai Bay) have also experienced a surge in leisure demand, of which the YRD market is the absolute market leader.

The skiing industry is booming in the run-up to the 2022 Winter Olympics: The skiing industry has witnessed a trend of mutual growth driven by supply and demand. On one hand, investment in outdoor ski destinations and indoor ski resorts is very active, which has driven the expansion of the novice skier market. Chongli, an important event host destination for the Beijing 2022 Winter Olympics, has seen strong growth in investment in infrastructure and ski resorts, and has become one of the most important ski destinations following the Northeast China.

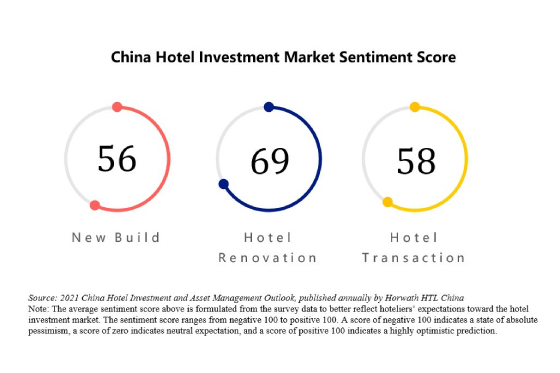

Construction of transportation infrastructure drives investment in new-build hotels:

The construction and expansion of new high-speed railway stations, new subway lines, new airports, and new integrated transportation hubs have brought many opportunities for the development and investment of hotels thanks to the expected large volume travelers generated by transportation hubs.

M&A outlook

In terms of M&A, we also note the following important trends:

Pure hotel asset M&As are less active: Hotel assets in China have quite lower investment returns due to relative lower ADR levels impacted by the supply pressure. Although there are still a considerable number of hotels in the market seeking to get out, it is difficult to reach a substantial deal due to the huge gaps in price expectation between buyers and sellers.

Restructuring and integration of hotel assets among SOEs: Most notably, China Rong Tong Group (CRTG) established China Rong Tong Tourism Development Group Co. (CRTTD) through the integration of military-run properties. CRTTD first consolidated more than 150 existing hotel assets, most of which are midscale and economy hotels.

The company is also responsible to renovate and upgrade hotel assets and establish an operating platform. But it will take time to see substantial progress as it is not easy to consolidate staff and interests of different parties. Some other large-scale SOEs are also consolidating their hotel business, including both assets and operating functions, to improve the operation efficiency and business performance.

Hotel operators seeking expansion through marriage with real estate groups: The most notable case is Yongle Huazhu, a new joint-venture platform established by Sunac China and Huazhu Hotels Group. The JV platform will take over Sunac’s investment projects of upper-midscale and above hotels that are currently under planning and development for the next five years, which might be beneficial to Huazhu for the presence and penetration in China’s upscale hotel market.